突发!“四大”某记一成员所因测评作弊被罚!

来源:四大新鲜事儿

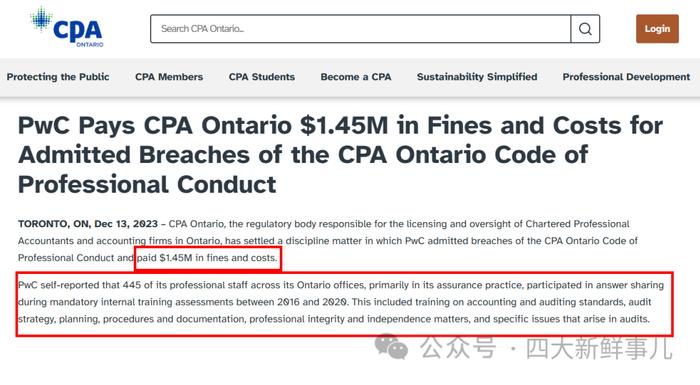

近日,加拿大安大略省注册会计师协会宣布与普华永道加拿大公司就一项违规事项达成了和解,和解金额为145万加元(约合人民币779万元),因为普华永道加拿大公司部分员工考核作弊,违反了安大略省注册会计师的行为准则。

一起来看看详细情况。

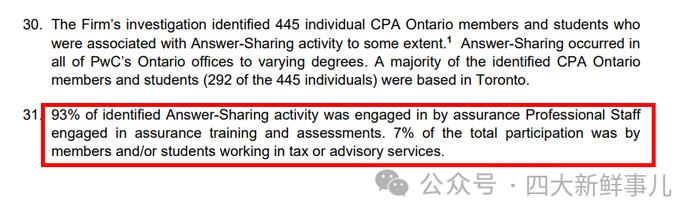

在2016年至2020年期间的强制性开放式内部培训评估中,普华永道加拿大公司445名专业人员(93%为审计员,7%为税务和咨询人员)参与了答案分享。此项培训包括会计和审计准则、审计战略、计划、程序和文件、职业操守和独立性以及审计中出现的具体问题等内容。

就在几周前,PCAOB宣布对普华永道中国内地和普华永道中国香港的欺诈行为处以总计700万美元的罚款。从2018年到2020年,普华永道香港的1000多名员工和普华永道中国内地的数百名员工,在与美国审计课程相关的强制性内部培训课程的在线测试中,通过两款未经授权的软件应用程序提供或获取答案,参与了不正当的答案共享。

当普华永道加拿大公司在2022年因作弊被PCAOB罚款时,有消息称,普华永道加拿大公司的员工在共享硬盘中存放了至少46项普华永道审计测试的答案。

这些人员主要通过使用专业人员在公司计算机网络上创建的几个共享驱动器(“共享驱动器”)共享答案,专业人员将答案发布在该驱动器上,供其他人查看并提供补充答案。此外,个人还可以通过发送包含培训试题答案附件的电子邮件、在硬拷贝文档中提供答案、或在其他人在场的情况下讨论答案等方式共享答案。

不当共享答案的情况主要发生在公司强制性鉴证培训的一部分测试中。在该事务所约55项强制性鉴证测试中,共享驱动器至少包含其中46项测试的答案。此外,共享驱动器还包括一些全事务所强制性测试的答案,其中包含有关职业操守和专业独立性的内容。

培训测试答案的不当分享涉及普华永道加拿大公司的初级员工、经理、董事和合伙人。公司领导层得知这一做法后,进行了内部调查。该事务所的调查显示,不当行为在该事务所的审计业务中普遍存在,包括受PCAOB标准管辖的审计人员。该公司鉴证业务中至少有1100名专业人员参与了答案共享。

加拿大安大略省注册会计师协会的公告也是这样说的:

具体来说,答案共享是通过以下方式进行的:

a.答案共享文件库创建于GoogleDrives上,一般可通过邀请访问。GoogleDrives是普华永道使用的GoogleWorkspace平台中的电子存储工具,其中包含文件夹和文档;

b.通过电子邮件文档创建和共享答案共享文档;

c.专业人员在现场培训课程结束时一起讨论答案。

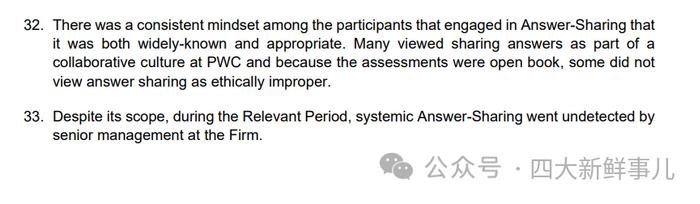

安大略省注册会计师协会的命令提到,普华永道加拿大公司对此事的态度是:答案共享是公司更大的“协作文化”的一部分,而不是将答案共享视为一件坏事。

参与答案共享的学员一致认为,答案共享是广为人知的,也是适当的。许多人认为共享答案是普华永道合作文化的一部分,而且由于评估是公开的,因此一些人认为共享答案在道德上并无不妥。

这种情况在2019年11月21日发生了变化,当时鉴证人员通过网络研讨会被告知需要“独立完成评估”。尽管有这一指示,一些专业人员在网络研讨会之后的一个多月里继续进行答案共享。

安大略省注册会计师协会称:

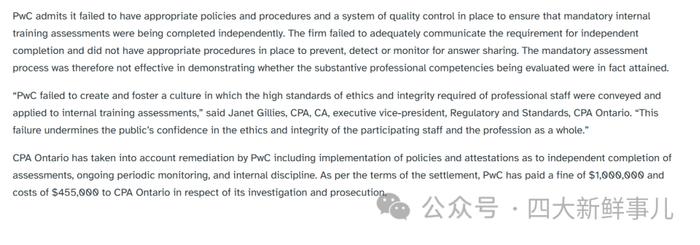

普华永道承认,它没有制定适当的政策、程序和质量控制体系,以确保员工独立完成强制性的内部培训评估。普华永道加拿大公司未能充分传达独立完成测评的要求,也没有适当的程序来防止、检测或监控答案共享。因此,强制性评估过程不能有效地证明所评估的实质性专业能力是否确实达到了。

从现在起,普华永道加拿大公司将定期对评估进行监督,以确保其独立完成。

我们不禁要问,除了监管者,还有谁会在乎一些过度工作的审计人员是否会在开放式的复选框评估中分享答案?

原英文报道如下:

Lastweek,CPAOntarioannouncedasettleddisciplinarymatterwithPwCCanada,thematterbeingcheatingandthesettlementbeing$1.45millionCAD($1.09millionUSD)infinesforbreachesoftheCPAOntariocodeofconduct.

Here’swhathappened.445professionalstaff—93percentauditorsandsevenpercenttaxandadvisory—participatedinanswersharingduringmandatory,open-bookinternaltrainingassessmentsbetween2016and2020.Thisincludedtrainingonaccountingandauditingstandards,auditstrategy,planning,proceduresanddocumentation,professionalintegrityandindependencematters,andspecificissuesthatariseinaudits.Despiteallthiswidespreadcheating,PwCCanadaactuallyhadacompletelyflawlessPCAOBinspectionreportin2020[PDF]soatleastsomeauditorsovertheremusthaveknownwhattheyweredoing.

EversinceKPMGwasfined$50millionbytheSECforcheatingin2019it’sbeenafree-for-allontheanswersharingpunishmentsaroundtheworld.EYUSgotfined$100millionbytheSECfordoingitin2022thoughtheirswasabitworseastheywerealsocheatingontheethicsexamsonemusttaketobelicensedasaCPAandnotjustWBLs.

Andjustafewweeksago,thePCAOBannounceditwasfiningPwCChinaandPwCHongKongatotalof$7millionUSDfortheirowncheating:From2018until2020,over1,000individualsfromPwCHongKong,andhundredsofindividualsfromPwCChina,engagedinimproperanswersharing–byeitherprovidingorreceivingaccesstoanswersthroughtwounauthorizedsoftwareapplications–inconnectionwithonlinetestsformandatoryinternaltrainingcoursesrelatedtothefirms’U.S.auditingcurriculum.

WhenPwCCanadawasfinedforcheatingbythePCAOBin2022,itwasrevealedPwCCanadapersonnelmaintainedshareddrivespackedwithanswerstoatleast46ofPwC’saudittests.Sowekindaalreadyknewtherewassomecheatinggoingonoverthere.

Fromatleast2016toearly2020,morethan1,200PwCCanadapersonnelwereinvolvedinimproperanswersharingrelatedtotrainingtests.FirmpersonnelprimarilysharedanswersthroughuseofseveralshareddrivesthatprofessionalshadcreatedontheFirm’scomputernetwork(the“SharedDrives”),andonwhichprofessionalshadpostedtheanswersforotherstoviewandprovidesupplementalanswers.Inaddition,individualssharedanswersbysendingemailswithattacheddocumentscontaininganswerstotrainingtestquestions,byprovidinganswersinhardcopydocuments,orbydiscussinganswerswhentakingtestsinthepresenceofothers.

InstancesofimproperanswersharingprimarilyoccurredinconnectionwithteststhatwereapartoftheFirm’smandatoryAssurancetraining.TheSharedDrivescontainedanswersforatleast46oftheFirm’sapproximately55mandatoryAssurancetests,aswellasanswersforsomemandatoryFirm-widetestscontainingcontentconcerningprofessionalintegrityandprofessionalindependence.

Impropersharingoftrainingtestanswersoccurredamongjuniorstaff,managers,directors,andpartnersattheFirm.AfterFirmleadershiplearnedofthepractice,itconductedaninternalinvestigation.TheFirm’sinvestigationrevealedthatthemisconductwaswidespreadwithintheFirm’sauditpractice,includingamongthosewhoperformedworkonauditsgovernedbyPCAOBstandards.Atleast1,100professionalsintheFirm’sAssurancepracticewereinvolvedinanswersharing.

AndtheCPAOntarioordersaysessentiallythesamething:

Specifically,Answer-Sharingoccurredinthefollowingways:

a.RepositoriesofAnswer-SharingDocumentswerecreatedonGoogleDrivesandgenerallyaccessiblebyinvitation.GoogleDrivesareelectronicstoragetoolswithintheGoogleWorkspaceplatformusedbyPwCthatcontainfoldersanddocuments;

b.Answer-SharingDocumentswerecreatedandsharedbyemaildocuments;and

c.ProfessionalStaffworkedtogetherattheendofin-persontrainingsessionsandreferred

collectivelytoAnswer-SharingDocuments.

TheCPAOntarioordermentionsthatratherthanseeinganswersharingasabadthing,theattitudeatPwCCanadawasthatanswersharingispartofagreater“collaborativeculture”atthefirm.

TherewasaconsistentmindsetamongtheparticipantsthatengagedinAnswer-Sharingthatitwasbothwidely-knownandappropriate.ManyviewedsharinganswersaspartofacollaborativecultureatPWCandbecausetheassessmentswereopenbook,somedidnotviewanswersharingasethicallyimproper.

ThatchangedonNovember21,2019whenassurancestaffweretoldviawebinarto“completeassessmentsindependently.”

Thecommunicationwasmotivatedbythepublicationofpressreleasesandnewsstoriesregardingadifferentfirm’smanipulationofitstrainingassessmentsysteminanotherjurisdictionandwasnotrelatedtoanyawarenessbytheFirmthatitsownProfessionalStaffhadbeenactivelyengaginginAnswer-SharingtothatpointintheRelevantPeriod.Despitethisinstruction,Answer-SharingamongstsomeProfessionalStaffcontinuedfollowingthewebinarforoveronemonth.

SaidCPAOntario:

PwCadmitsitfailedtohaveappropriatepoliciesandproceduresandasystemofqualitycontrolinplacetoensurethatmandatoryinternaltrainingassessmentswerebeingcompletedindependently.Thefirmfailedtoadequatelycommunicatetherequirementforindependentcompletionanddidnothaveappropriateproceduresinplacetoprevent,detectormonitorforanswersharing.Themandatoryassessmentprocesswasthereforenoteffectiveindemonstratingwhetherthesubstantiveprofessionalcompetenciesbeingevaluatedwereinfactattained.

“PwCfailedtocreateandfosteracultureinwhichthehighstandardsofethicsandintegrityrequiredofprofessionalstaffwereconveyedandappliedtointernaltrainingassessments,”saidJanetGillies,CPA,CA,executivevice-president,RegulatoryandStandards,CPAOntario.“Thisfailureunderminesthepublic’sconfidenceintheethicsandintegrityoftheparticipatingstaffandtheprofessionasawhole.”

Fromnowon,PwCCanadawillengageinperiodicmonitoringofassessmentstoensuretheyarecompletedindependently.AndPwCCanada’sjuniorauditorswilllearntokeepthisthingeveryonedoesonthedown-lowgoingforward.

Wefeelcompelledtoask—doesanyoneotherthanregulatorsgiveashitifsomeoverworkedauditorsshareanswersonopenbook,checkboxassessments?Truly?