优化地方政府债券信息披露研究(附英文版)

摘 要

信息披露制度是地方政府债券市场稳健运行的重要保障。本文在梳理地方债信息披露现状的基础上,对地方债信息披露的现实效应进行实证检验,发现提升地方债信息披露质量有助于降低债券发行利差、提升二级市场的流动性水平。进一步就国内外地方债信息披露的内容和平台进行对比,发现我国地方债信息披露水平已取得长足进展。为进一步完善地方债信息披露制度,本文提出丰富地方债信息披露内容、构建统一的信息披露标准、完善信息披露平台功能等建议。

关键词

地方政府债券 信息披露 披露规范

地方政府债券(以下简称“地方债”)是落实财政政策的重要抓手,在稳定宏观经济中发挥着重要作用。信息披露机制能够降低发行人与投资者之间的信息不对称、提升债券市场的运行效率,是实现地方债市场健康发展的重要保障。近年来,中央一直高度重视地方政府债务管理和信息公开,在此背景下,本文通过梳理地方债信息披露发展状况、实证检验地方债信息披露实际作用、对比分析地方债信息披露内容和平台功能,提出优化地方债信息披露的政策建议,以期助力我国地方债信息披露制度建设,推动政府债券市场高质量发展。

地方债信息披露政策演进与平台建设

(一)政策演进

自地方债自发自还试点以来,在顶层设计和相关政策规定的指导下,地方债信息披露机制逐步建立。2014年,国务院发布《关于加强地方政府性债务管理的意见》,将地方政府债务公开制度与加强政府信用体系建设联系起来。同年,财政部发布《关于2014年地方政府债券自发自还试点信息披露工作的指导意见》,为地方债信息披露的规则制定奠定基础。2018年,财政部发布《地方政府债务信息公开办法(试行)》,要求地方债信息公开,必须“突出重点,真实、准确、完整、及时公开”。2019年12月,《关于启用地方政府新增专项债券项目信息披露模板的通知》发布,地方政府专项债券的信息披露要求更为细化。2021年,国务院印发《关于进一步深化预算管理制度改革及意见》,将“健全地方政府债务信息公开及债券信息披露机制,发挥全国统一的地方政府债务信息公开平台作用”作为防范化解地方政府债务风险的重要措施。目前,地方债信息披露已经形成较完整的政策框架,各地信息披露文件较全面,披露指标存在个别差异。

(二)平台建设

地方债信息披露平台建设日益完善。目前进行地方债信息披露的平台主要包括中国地方政府债券信息公开平台(以下简称“地方债信息平台”)和中国债券信息网(以下简称“中债信息网”)。地方债信息平台于2019年启用,是财政部对外统一发布地方政府债务信息,服务社会公众的唯一网络窗口。中债信息网创办于1998年,是由中央结算公司主办、向国内外用户提供债券市场信息服务的专业网站,也是中国人民银行指定的全国银行间债券市场信息披露官方平台。目前,两个平台均能提供地方债的信息披露文件和统计数据。

提升地方债信息披露质量的现实效应

(一)理论分析

1.提升信息披露质量有助于降低债券发行成本

依据信息不对称理论,发行人与投资者之间天然存在信息不对称。当投资者无法完全掌握发行人信息的时候,其倾向于要求更高的债券收益率以弥补潜在风险,从而导致发行人融资成本抬升。因此,提高地方债信息披露质量,有助于投资者充分了解地方财政状况和募投项目信息、提升投资者对发行人的信赖程度,从而缩小地方债的信用利差,降低发行成本。

2.提升信息披露质量有助于提升债券流动性

债券收益率与发行人风险水平呈正相关,发行人有动机隐瞒自身负面信息,导致投资者不能准确评估债券价值。依据信号传递理论,信息披露有助于形成外部监督机制,促使优质发行人通过信息披露揭示自身潜在价值。投资者了解到这一动机后,认为信息披露质量高的债券能以相对公平的价格进行交易,在交易时会优先选择信息披露质量高的债券,从而提升此类债券的流动性。

(二)实证检验

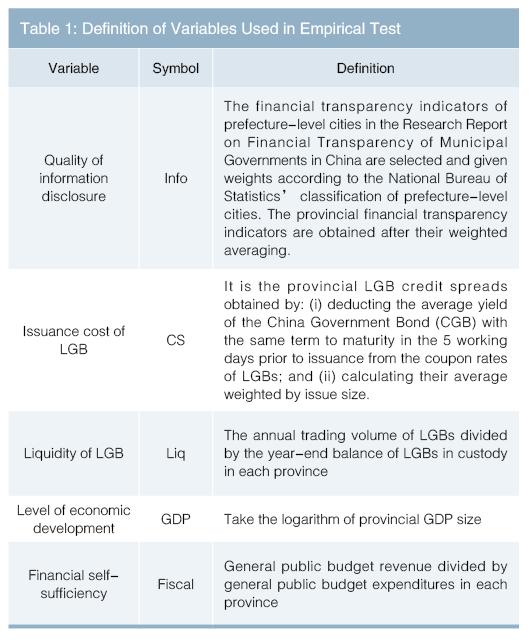

本部分使用2015—2021年各省份数据,实证检验信息披露质量对地方债发行成本和流动性的影响。数据来源为万得(Wind)数据库和中国地方政府债券信息公开平台。本文以各省份信息披露质量为自变量,以地方债信用利差和换手率为因变量,在控制各省经济发展水平和财政自给程度的条件下,探究信息披露质量对地方债发行成本和流动性的影响。实证检验所使用的变量定义如表1所示。

依据上述变量,构建回归方程如下:

CSit=α0+α1Infoit+α2GDPit+α3Fiscalit+εit (1)

Liqit=α0+α1Infoit+α2GDPit+α3Fiscalit+εit (2)

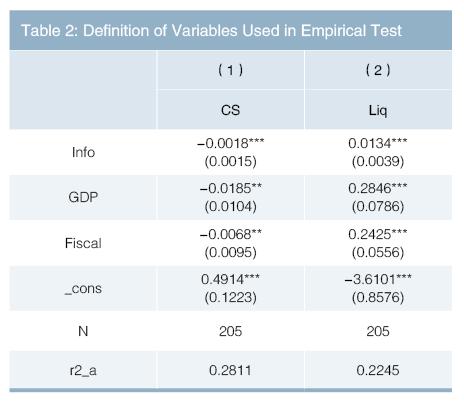

回归方程中,i代表省份,t代表年份,残差εit代表其他影响因素。方程(1)中的系数α1代表信息披露对地方债发行成本的影响,方程(2)中的系数α1代表信息披露对地方债流动性的影响。回归结果如表2所示。

表2中第(1)(2)列分别是方程(1)和方程(2)的回归结果。结果显示,地方债信息披露质量与地方债发行成本存在显著的负相关关系,信息披露质量较高的省份,其地方债发行成本较低;地方债信息披露质量与地方债流动性存在显著的正相关关系,信息披露质量越高的省份,其地方债的流动性水平越好。实证结果验证了前文的理论分析,说明提升地方债信息披露质量,有助于降低发行人与投资者人之间的信息不对称,从而降低地方债一级市场发行成本,提升地方债在二级市场的流动性水平。

地方债信息披露比较分析

(一)地方债信息披露内容比较

目前我国地方债信息披露内容主要包括发行前信息披露及存续期信息披露。发行前信息披露主要包括发行通知、信息披露文件、信用评级、专项债的“一案两书”1、新增专项债的信息披露模板和再融资债券的公开发行文件。存续期信息披露文件主要包括还本付息公告、财政经济债务相关数据、存续期公开、机构跟踪评级报告以及新增专项债券存续期信息披露模板。本文主要对不同发行人信息披露存在差异的内容进行分析比较。

1.境内地方债信息披露比较

第一,在发行前的信息披露中,信用评级报告内容有明显差异,容易体现出区域优势。从各发行人实际披露内容来看,信用评级报告要包括主体概况、宏观经济与政策环境分析、区域经济实力、政府治理水平、财政实力、债务状况和本期债券偿还能力。不同发行人之间的内容差异主要体现在地区经济特色方面,例如山东省突出其良好的制造业基础和海洋经济优势,山西省则侧重对于煤炭资源和经济转型方面的介绍。具备地方特色的信用评级报告有助于发行人体现自身优势,吸引相关领域投资者。

第二,发行前信息披露文件存在明显差异,其包含地方债信息最多,主要包括债券概况、信用评级结果、地区经济、财政状况和债务情况。目前发行人信息披露文件主要涵盖近3年的一般公共预算、转移支付、地方债、政府性基金和国有资本经营的收入和支出数据。披露质量较高的信息披露文件体现在三方面:一是在政府债务状况的介绍中,将债务按层级、资金投向、到期时间进行数据披露;二是披露当地《国民经济和社会发展五年规划》等文件,有助于投资者了解当地长期宏观规划;三是在一般债券的募集资金投向方面,说明资金的具体用途,具体到每一个项目的名称和使用额度。

第三,存续期信息披露质量存在较大差异。在地方债存续期间信息披露文件包括地方经济财政数据、债券存续基本情况、跟踪评级报告和新增专项债信息披露模板。除还本付息公告外,并非所有地区发行人都会公开披露其余文件。而披露质量较高的地区,如上海市,存续期披露文件还对债券投向的项目名称、建设进度和运营情况进行披露,使市场对募集资金使用和项目建设情况有详细了解,有助于提升投资者对发行人的信心。

2.境内与离岸地方债信息披露比较

2021年以来,广东省、深圳市、海南省相继发行11只离岸人民币地方债,并按照境外市场的相关要求进行信息披露。总体而言,境外要求对于规则性的解释和说明更详细,境内要求在新增专项债信息披露方面的介绍更丰富。

信息披露顶层设计方面,由香港交易所、中华(澳门)金融资产交易股份有限公司(MOX)等基础设施机构出台相关规范文件,约束力度较境内偏弱。信息披露规范方面,信息披露文件围绕单次发行展开,在承销商和律师事务所等中介机构的协助下,会尽可能整合包括统领性规则在内的全部相关信息。

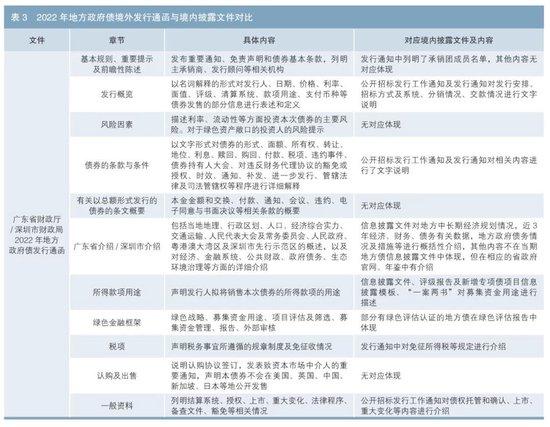

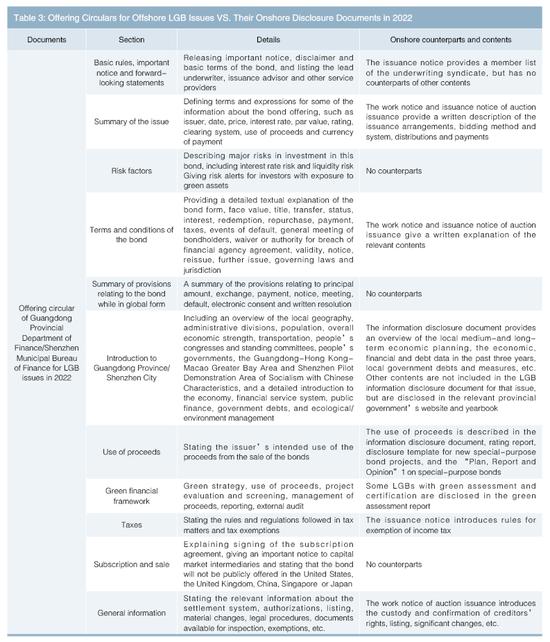

发行前信息披露方面,从完整性来看,境外相较于境内多披露了部分条款规则及声明等内容,少披露了募投项目信息情况,对于绿色项目额外披露绿色金融框架信息。披露内容方面,境内地方债发行需披露信用评级报告、信息披露文件、发行计划、专项债“一案两书”等文件。广东省、深圳市政府于2021—2022年分别赴澳门、香港发行地方债,均公开发布发行通函文件,较为详细地介绍了发行人情况、债券信息、发行条款、风险提示等重要内容。其具体结构特点,及其与对应境内披露文件内容的对比见表3。

发行主体信息披露包含披露指标和文字描述。从披露指标来看,境内外发行主体均披露地方经济状况、财政收支和地方政府债务状况三类指标。境内地方债与主体相关的披露指标数量低于离岸地方债,离岸地方债发行主体对一般公共预算的收入明细和支出项、货物贸易进出口指标、税收收入及非税收收入的明细科目进行了详细披露。从文字描述来看,离岸地方债信息披露还增加了部分政策和数据的描述,如需补充生态环境治理和对外交流的相关描述。

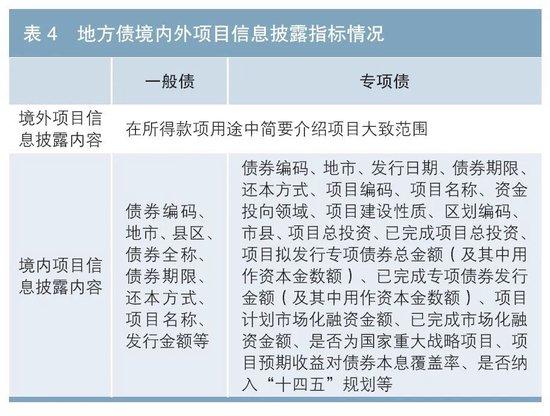

项目信息披露方面,境内地方债较离岸地方债更为详细。境内地方债将项目情况以表格形式列明各项信息,离岸地方债则未进行详细描述。境内外地方债项目信息披露指标对比如表4所示。

存续期信息披露方面,深圳市公开发布了《2021年深圳市离岸人民币地方政府绿色债券募集资金使用情况报告》,披露2021年发行的39亿元绿色债券的项目分类、市区划分、项目名称、项目金额等募集资金投向信息。广东省、海南省及深圳市发行的其他离岸债券暂无存续期的信息披露。

3.地方债信息披露内容国际比较

关于地方债信息披露内容的国际比较,近期已有较为成熟的研究成果。根据相关文献,信息披露内容的差异是法律制度、会计制度、市场发展阶段、市场现状等多种因素共同作用的结果。在发行主体信息方面,我国侧重披露地区宏观经济数据,而美国更侧重对微观财务信息的披露;在专项债券的信息披露中,我国信息披露的精细化程度已高于美国。

(二)地方债信息披露平台比较

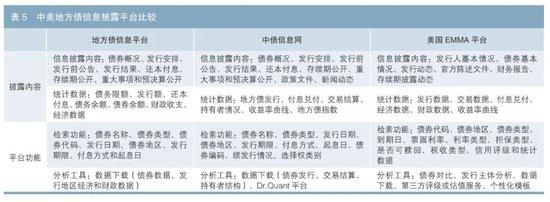

我国地方债信息披露内容主要发布在地方债信息平台和中债信息网,美国市政债券信息披露官方网站为EMMA平台。以下从平台的披露内容和平台功能两方面对两国信息披露平台进行对比。

1.披露内容方面

信息方面,我国的信息披露平台主要披露债券概况、发行安排、发行前公告、发行结果、还本付息、存续期公开、重大事项和预决算公开,中债信息网还额外收录了中央及地方相关政策文件和地方债新闻动态。美国EMMA平台市政债信息包括发行人基本情况、债券基本情况、发行动态、官方陈述文件、财务报告和存续期披露动态等板块。

统计数据方面,地方债信息平台主要涵盖债务限额、发行额、还本付息、债务余额、债券余额、一级市场发行、财政收支和经济社会发展等数据;中债信息网则提供地方债发行、付息兑付、交易结算、持有者情况等统计信息,同时收录收益率曲线、地方债指数等估值数据。美国EMMA平台提供市政债发行数据、交易数据、地方政府经济财政数据和收益率曲线等数据指标。

2.平台功能方面

在检索功能方面,地方债信息平台和中债信息网均可通过关键字检索信息披露文件。对于统计数据,地方债信息平台和中债信息网均未提供检索功能,两平台都需要使用下拉菜单选择数据指标或下载统计报表。美国EMMA平台提供的债券搜索条件包括债券代码、债券地区、债券类型、到期日、票面利率、利率类型、担保类型、是否可赎回、税收类型、信用评级。对于统计数据,网页可进行数据指标的搜索。

在分析工具方面,地方债信息平台提供债券数据、发行地区经济和财政数据的下载,中债信息网在网页端提供债券发行、交易结算、持有者结构等总量统计数据的下载功能。需要更详细数据和分析则需下载中债Dr.Quant金融终端等产品。Dr.Quant提供各省份的地方债发行、交易、存量、收益率曲线和期限结构等分析工具,是目前国内信息最全的地方债分析工具。美国EMMA平台的工具种类丰富,在债券对比功能中,提供债券基本要素、市场价格、交易数据等信息的比较;在发行主体分析功能中,提供发行主体的联系信息、历史发行情况、信用评级等信息;在外部拓展工具方面,投资者可以查看有关债券的第三方服务,如穆迪、惠誉评级、标准普尔等机构对债券的信用评级,以及第三方提供商提供的市政债券市场收益率曲线和指数。

地方债信息披露优化建议

根据前文分析,本文提出如下地方债信息披露的优化建议。

(一)丰富地方债信息披露内容

提升信息披露质量能够降低地方债融资成本、提升地方债流动性。我国部分地区在信息披露精细程度上有待提升。建议相关发行人丰富地方债披露信息,增加例如项目完工百分比、款项使用情况、环境效益指标等信息,以高质量信息披露降低融资成本。

(二)构建统一的信息披露标准

在地方债实际披露中,地区之间披露详细程度有所差异,境内与离岸债披露内容亦有不同。因此,建议进一步完善相关法律法规,构建统一的地方债信息披露标准,设计细化的信息披露填报模板,提升地方债信息披露的一致性和可比性。

(三)完善信息披露平台功能

我国地方债信息披露平台功能还存在进一步完善的空间。建议增加信息披露平台功能,补充权威第三方机构的收益率曲线、价格指标等信息的展示,方便投资者分析决策。

注:

1.一案两书,即《专项债券项目实施方案》《项目财务评价报告书》和《项目法律意见书》。

参考文献

[1]姚东旻,罗文淇.地方政府债券信息披露比较研究与优化设计[J].债券,2023(1):31-38.DOI:10.3969/j.issn.2095-3585.2023.01.008.

[2]时心怡,陈素云.优化地方债信息披露的现实基础与实现路径[J].财会通讯,2022(20):14-19.DOI:10.16144/j.cnki.issn1002-8072.2022.20.018.

◇ 本文原载《债券》2023年7月刊

◇ 作者:中央结算公司博士后科研工作站 杜通

中央结算公司深圳分公司 李东升

◇编辑:廖雯雯 鹿宁宁

ResearchonOptimizingInformationDisclosureofLocalGovernmentBonds

DuTong,LiDongsheng

Abstract

Theinformationdisclosuresystemispivotaltothesoundnessofthelocalgovernmentbond(LGB)market.BasedonareviewofthestatusquoofLGBinformationdisclosure,thispaperempiricallyteststhepracticaleffectsofLGBinformationdisclosureandfindsthathigherqualityofLGBinformationdisclosurehelpsreducethebondspreadsandboosttheliquidityofthesecondarymarket.AfurthercomparisonofthecontentsandplatformsofLGBinformationdisclosureathomeandabroadshowsgreatprogressinChina’sLGBinformationdisclosure.InordertofurtherimprovetheLGBinformationdisclosuresystem,thispaperproposestoenrichthecontentofLGBinformationdisclosure,unifythestandardsforLGBinformationdisclosureandimprovethedisclosureplatformfunctions.

Keywords

Localgovernmentbonds,informationdisclosure,disclosurestandards

Localgovernmentbonds(“LGBs”)areanimportantinstrumentforimplementingfiscalpolicy,playinganimportantroleinstabilizingthemacro-economy.Theinformationdisclosuremechanismreducestheinformationasymmetrybetweentheissuerandtheinvestors,improvesthebondmarketefficiencyandservesasapillarforhealthydevelopmentoftheLGBmarket.Inrecentyears,theCentralGovernmenthasalwaysattachedgreatimportancetotheLGBmanagementanddisclosure.Againstthebackdrop,thispaperprovidespolicyrecommendationsforimprovingLGBinformationdisclosureafterreviewingdevelopmentsinLGBinformationdisclosure,empiricallytestingtheactualroleofLGBinformationdisclosureandcomparativelyanalyzingthecontentsandplatformfunctionsofLGBinformationdisclosure,soastohelpbuildChina’sLGBinformationdisclosuresystemandpursuehigher-qualitydevelopmentofthegovernmentbondmarket.

EvolutionofLGBInformationDisclosurePolicyandPlatform

i.Policyevolution

SincethepilotschemeofLGBself-issuanceandself-repaymentbegan,theLGBinformationdisclosuremechanismhasbeengraduallyestablishedundertheguidanceoftop-leveldesignandrelevantpolicies.In2014,theStateCouncilissuedtheGuidelinesforStrengtheningManagementofLocalGovernmentDebts,linkingthelocalgovernmentdebtdisclosuresystemtoenhancingthegovernmentcreditabilitysystem.Inthesameyear,theMinistryofFinanceissuedtheGuidanceonInformationDisclosureforthePilotSchemeonSelf-issuanceandSelf-repaymentofLocalGovernmentBondsin2014,layingthefoundationfordevelopingrulesonLGBinformationdisclosure.In2018,theMinistryofFinanceissuedtheMeasuresforInformationDisclosureofLocalGovernmentBonds(forTrialImplementation),requiringthedisclosureofLGBinformationtobe“focused,true,accurate,completeandtimely”.InDecember2019,theNoticeonLaunchingtheInformationDisclosureTemplateforLocalGovernment’sNewSpecial-purposeBondProjectswasissued,furtherrefiningtheLGBinformationdisclosurerequirements.In2021,theStateCouncilissuedtheSuggestionsonFurtherDeepeningtheReformofBudgetManagementSystem,whichregards“improvingthemechanismsfordisclosinglocalgovernmentdebtinformationandbondinformationandgivingfullplaytotheroleofaunifiednationalplatformfordisclosinglocalgovernmentdebtinformation”asanimportantmeasuretoforestallanddefusethelocalgovernmentdebtrisk.Atpresent,acompletepolicyframeworkforLGBinformationdisclosurehastakenshape,withafullrangeofdisclosuredocumentspublishedbylocalgovernments,whichusedisclosureindicatorsthatareslightlydifferent.

ii.Platformdevelopment

TheLGBinformationdisclosureplatformhasbeenincreasinglyimproved.Atpresent,theplatformsforLGBinformationdisclosuremainlyincludetheChinaElectronicLocalGovernmentBondMarketAccess(“CELMA”)andthewebsitewww.ChinaBond.com.cn(“ChinaBond.com.cn”).CELMAwaslaunchedin2019astheonlyonlinewindowfortheMinistryofFinancetoreleaseLGBinformationtothepublic.Foundedin1998,ChinaBond.com.cnisaspecializedwebsitesponsoredbyCCDC.Itprovidesbondmarketinformationservicestodomesticandforeignusers.ItisalsoanofficialplatformdesignatedbythePeople’sBankofChinaforinformationdisclosureinthenationalinter-bankbondmarket.Atpresent,bothplatformsprovideinformationdisclosuredocumentsandstatisticsofLGBs.

PracticalEffectsofImprovingtheQualityofLGBInformationDisclosure

i.Theoreticalanalysis

1.Higher-qualitydisclosurehelpsreducethecostsofbondissuance

Accordingtotheinformationasymmetrytheory,informationasymmetrynaturallyexistsbetweentheissuerandtheinvestors.Whentheissuerinformationisnotfullyavailable,investorstendtodemandhigherbondyieldstocompensateforpotentialrisks,resultinginhigherfinancingcostsfortheissuer.Therefore,improvingthequalityofLGBinformationdisclosurehelpsinvestorsfullyunderstandthefinancialpositionoflocalgovernmentsandtheinformationonfinancedprojects,enhanceinvestors’trustintheissuer,narrowthecreditspreadsofLGBs,andlowertheissuancecost.

2.Higher-qualitydisclosurehelpsboosttheliquidityofbonds

Thebondyieldispositivelycorrelatedwiththeriskleveloftheissuer.Theissuerismotivatedtoconcealitsownnegativeinformation,preventinginvestorsfromaccuratelyassessingthebondvalue.Accordingtothetheoryofsignaltransmission,informationdisclosurefostersanexternalsupervisionmechanismthatencourageshigh-qualityissuerstorevealtheirpotentialvaluethroughinformationdisclosure.Afterbecomingawareofthismotivation,investorsbelievethatbondswithhigherdisclosurequalitycanbetradedatamorefairprice,andbondswithhigherdisclosurequalitywillbepreferredintrading,thusimprovingtheliquidityofsuchbonds.

ii.Empiricaltesting

Thissectionusesprovincialdatabetween2015and2021toempiricallytesttheeffectsofinformationdisclosurequalityontheissuancecostandliquidityofLGBs.ThedatasourcesareWinddatabaseandCELMA.ThispapertakesthequalityofinformationdisclosureineachprovinceastheindependentvariableandthecreditspreadsandturnoverrateofLGBsasthedependentvariables,andexplorestheeffectsofdisclosurequalityontheissuancecostandliquidityofLGBsundertheconditionofcontrollingtheeconomicdevelopmentlevelandfinancialself-sufficiencyofeachprovince.ThevariablesusedintheempiricaltestaredefinedinTable1.

Basedontheabovevariables,aregressionequationisgivenasfollows:

CSit=α0+α1Infoit+α2GDPit+α3Fiscalit+εit (1)

Liqit=α0+α1Infoit+α2GDPit+α3Fiscalit+εit (2)

Intheregressionequation,irepresentsprovince,trepresentsyear, andtheresidualεit representsotherinfluencingfactors. Thecoefficienta1inequation(1)representstheimpactofinformationdisclosureontheissuancecostofLGBs,andthecoefficienta1 inequation(2)representstheimpactofinformationdisclosureontheliquidityofLGBs.TheregressionresultsareshowninTable2.

Columns(1)and(2)inTable2representtheregressionresultofEquation(1)andEquation(2),respectively.TheresultsshowthatthereisasignificantnegativecorrelationbetweenthequalityofLGBinformationdisclosureandthecostofLGBissuance.TheprovinceswithahigherqualityofinformationdisclosurehavelowercostofLGBissuance.ThereisasignificantpositivecorrelationbetweenthequalityofLGBinformationdisclosureandtheliquidityofLGB.Thehigherthequalityofinformationdisclosure,thebettertheliquidityofLGB.Theempiricaltestingresultsverifytheprevioustheoreticalanalysis,indicatingthatimprovingthequalityofLGBinformationdisclosurehelpsreducetheinformationasymmetrybetweentheissuerandtheinvestors,thusreducingthecostofLGBissuanceintheprimarymarketandboostingtheliquidityofLGBsinthesecondarymarket.

ComparativeAnalysisonLGBInformationDisclosure

i.ComparisonofContentsofLGBInformationDisclosure

Atpresent,theLGBinformationdisclosureinChinamainlyincludespre-issuedisclosureandpost-issuedisclosure.Thepre-issuedisclosuremainlyincludestheofferingcircular,informationdisclosuredocuments,creditrating,the“Plan,ReportandOpinion”1onspecial-purposebonds,theinformationdisclosuretemplatefornewspecial-purposebondsandthepublicofferingdocumentsoftherefinancingbonds.Thepost-issuedisclosuredocumentsmainlyincludetheannouncementofprincipalredemptionandinterestpayments,thefinancial,economicanddebtdata,ongoingdisclosure,follow-upratingreportsofratingagenciesandthedisclosuretemplatefornewspecial-purposebonds.Thispapermainlyanalyzesandcomparesthedifferentcontentsofinformationdisclosurebydifferentissuers.

1.ComparisonofonshoreLGBinformationdisclosures

First,inthepre-issuedisclosure,thereareobviousdifferencesinthecontentsofcreditratingreports,whicheasilyreflecttheregionaladvantages.Asshownbywhattheissuershavedisclosed,thecreditratingreportshouldincludetheissuerprofile,analysisofmacroeconomicandpolicyenvironment,regionaleconomiccapacity,localgovernment’sgovernancecapacity,localfinancialposition,localdebtstatusanddebtserviceabilityforthebondissue.Thedifferencesindisclosurecontentbetweenissuersaremainlyintheregionaleconomiccharacteristics.Forexample,ShandongProvincehighlightsitsstrongmanufacturingbaseandmarineeconomicadvantages,whileShanxiProvincefocusesitsprofileoncoalresourcesandeconomictransformation.Creditratingreportswithlocalcharacteristicshelptheissuershowcaseitsstrengthsandattractinvestorsinrelevantfields.

Second,therearesignificantdifferencesinthepre-issuedisclosuredocuments,whichcontainthemostLGBinformation,mainlyincludingthebondprofile,creditratingresults,regionaleconomy,localfinancialpositionandlocaldebtstatus.Atpresent,theissuer’sinformationdisclosuredocumentsmainlycoverthegeneralpublicbudget,transferpayments,LGBs,governmentfundsandrevenueandexpendituredataofthestate-ownedcapitaloperationsinthepastthreeyears.Higher-qualitydisclosuredocumentsshowthreecharacteristics:Firstly,thegovernmentdebtprofiledisclosesdataontiers,useoffundsandduedatesofdebts.Secondly,thelocalgovernment’sFive-YearPlanforEconomicandSocialDevelopmentandotherdocumentsaredisclosedtohelpinvestorsunderstandthelocallong-termmacro-planning.Thirdly,intermsoftheutilizationofproceedsfromgeneral-purposebonds,theproject-specificutilizationandquotaarestated.

Third,therearesignificantdifferencesinthequalityofpost-issuedisclosure.Thepost-issuedisclosuredocumentsofLGBsincludelocaleconomicandfinancialdata,basicdetailsofoutstandingbonds,follow-upratingreportsanddisclosuretemplatesfornewspecial-purposebonds.Notallregionswillseetheissuersdisclosedocumentsotherthantheannouncementofprincipalredemptionandinterestpayments.Inregionswithhigherdisclosurequality,suchasShanghai,thepost-issuedisclosuredocumentsalsodisclosethename,progressandoperatingconditionsoftheprojectfundedbythebondproceeds,providemarketparticipantswithaccesstodetailedinformationontheuseofraisedfundsandunderlyingprojectsandthushelpenhanceinvestors’confidenceintheissuers.

2.ComparisonofonshoreandoffshoreLGBinformationdisclosures

Since2021,GuangdongProvince,ShenzhenCityandHainanProvincehaveissued11offshoreRMBLGBsanddisclosedinformationinaccordancewithapplicableoffshoremarketrules.Onthewhole,offshorerequirementsprovideamoredetailedexplanationofrules,whileonshorerequirementsprovidemoreinformationaboutthedisclosureofnewspecial-purposebonds.

Asforthetop-leveldesignofdisclosure,theHongKongStockExchange,Chongwa(Macao)FinancialAssetExchangeCo.,Ltd.(MOX)andotherfinancialmarketinfrastructures(FMIs)haveissuedrelevantnormativedocuments,whicharelessbindingthanthoseintheonshoremarket.Intermsofdisclosurestandards,disclosuredocumentsarespecifictoindividualbondissues.Withassistancefromintermediariessuchasunderwritersandlawfirms,allrelevantinformation,includingoverarchingrules,willbeintegratedasmuchaspossible.

Intermsofpre-issuedisclosure,fromtheperspectiveofdisclosurecompleteness,offshoreissuersdisclosemoreterms,rulesandstatementsandlessinformationaboutfundedprojectsthantheironshorecounterparts.Forgreenprojects,additionalinformationaboutthegreenfinanceframeworkisdisclosed.Intermsofdisclosurecontent,thedisclosureofLGBsissuedonshoreincludescreditratingreports,informationdisclosuredocuments,issuanceplanandthe“Plan,ReportandOpinion”1onspecial-purposebonds.TheGuangdongprovincialgovernmentandtheShenzhenmunicipalgovernmentissuedLGBsinMacaoandHongKongrespectivelyfrom2021to2022.Bothofthempublishedofferingcircularsprovidingimportantdetails,includingtheissuerprofile,bondinformation,termsofissueandriskalerts.SeeTable3forspecificstructuralfeaturesoftheofferingcircularandcomparisonwithitsonshorecounterpart.

Theissuerinformationdisclosureincludesdisclosureindicatorsandtextualdescription.Asfordisclosureindicators,bothonshoreandoffshoreissuersdisclosethreetypesofindicators:localeconomicconditions,publicrevenueandexpenditureandlocalgovernmentdebtstatus.Therearelessissuer-relateddisclosureindicatorsforonshoreLGBsthanthoseforoffshoreLGBs.TheoffshoreLGBissuerdisclosesindetailthegeneralpublicbudgetrevenueandexpenditureitems,importandexportindicatorsoftradeingoods,taxrevenueandnon-taxrevenue.Asfortextualdescription,theoffshoreLGBinformationdisclosurealsoaddssomedescriptionofpoliciesanddata,suchasthedescriptionofecologicalenvironmentmanagementandexternalexchanges.

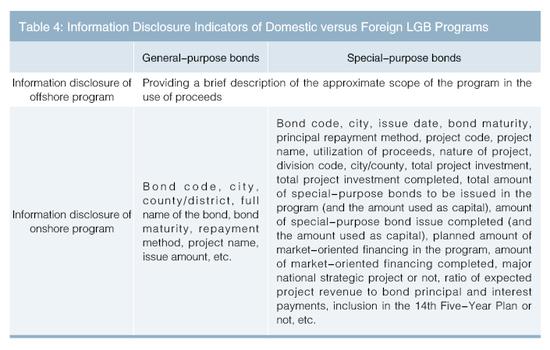

Asforprojectinformationdisclosure,onshoreLGBdisclosureismoredetailedthanoffshoreLGBdisclosure.TheonshoreLGBdisclosurepresentsitemizedprojectinformationintabularform,whiletheoffshoreLGBdisclosureprovidesnodetaileddescription.TheinformationdisclosureindicatorsofonshoreversusoffshoreLGBprojectsareshowninTable4.

Intermsofpost-issuedisclosure,ShenzhenCityhasissuedtheReportontheUseofProceedsfromOffshoreRMBGreenLGBsinShenzhenCityin2021,disclosingtheinformationontheprojectclassification,urbandivision,projectname,projectsize,etc.oftheRMB3.9billionworthofgreenbondsissuedin2021.Post-issuedisclosureistemporarilyunavailableforotheroffshorebondsissuedbyGuangdongProvince,HainanProvinceandShenzhenCity.

3.InternationalComparisonofLGBInformationDisclosure

Recently,therehavebeenmatureresearchresultsontheinternationalcomparisonofLGBinformationdisclosures.Accordingtorelevantdocuments,thedifferencesininformationdisclosurearetheresultofvariousfactors,suchaslegalsystem,accountingsystem,marketdevelopmentstageandmarketsituation.Intermsofissuerinformation,Chinafocusesonthedisclosureofregionalmacroeconomicdata,whiletheUnitedStatesfocusesmoreonthedisclosureofmicro-financialinformation.Intheinformationdisclosureofspecial-purposebonds,China’sinformationdisclosureismoredetailedthanthatoftheUnitedStates.

ii.ComparisonofLGBinformationdisclosureplatforms

China’sLGBinformationisdisclosedmainlyonCELMAandChinaBond.com.cn,whiletheUSmunicipalbondinformationisdisclosedmainlyonEMMA.BelowisacomparisonoftheinformationdisclosureplatformsinChinaandtheUnitedStatesintermsofdisclosurecontentandplatformfunctions.

1.Disclosurecontent

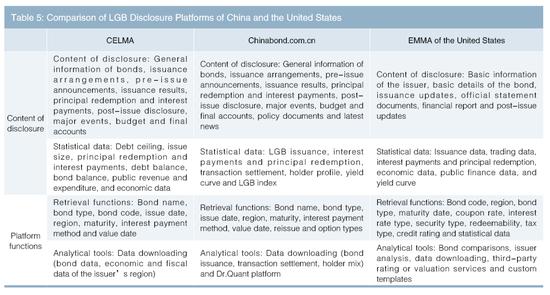

Intermsofinformation,China’sinformationdisclosureplatformmainlydisclosesthegeneralinformationofbonds,issuancearrangements,pre-issueannouncements,issuanceresults,principalredemptionandinterestpayments,post-issuedisclosure,majorevents,budgetandfinalaccounts.ChinaBond.com.cnadditionallyprovidesrelevantcentralandlocalpolicydocumentsandthelatestLGBnews.TheUnitedStates’EMMAmunicipalbonddisclosureincludesbasicinformationoftheissuer,basicdetailsofthebond,issuanceupdates,officialstatementdocuments,financialreportandpost-issueupdates.

Intermsofstatisticaldata,CELMAmainlycoversdatasuchasdebtceiling,issuesize,principalredemptionandinterestpayments,debtbalance,bondbalance,primarymarketissuance,publicrevenueandexpenditure,andeconomicandsocialdevelopment.ChinaBond.com.cnprovidesstatisticalinformationsuchasLGBissuance,interestpaymentsandprincipalredemption,transactionsettlementandholderprofile,andalsopublishesvaluationdatasuchasyieldcurvesandLGBindices.TheUnitedStates’EMMAplatformprovidesdataindicatorssuchasmunicipalbondissuancedata,tradingdata,localgovernments’economicandfinancialdataandyieldcurves.

2.Platformfunctions

Intermsofretrieval,bothCELMAandChinaBond.com.cnallowkeywords-basedretrievalofinformationdisclosuredocuments.Forstatisticaldata,neitherCELMAnorChinaBond.com.cnprovidesretrievalfunction,andbothplatformsrequireuseofthedrop-downmenutoselectdataindicatorsordownloadingofstatisticalreports.ThebondsearchtermsofferedbytheUSEMMAplatformincludebondcode,region,bondtype,maturitydate,couponrate,interestratetype,securitytype,redeemability,taxtype,andcreditrating.Asforstatisticaldata,webpagesallowsearchesfordataindicators.

Intermsofanalyticaltools,CELMAprovidesdownloadingofbonddata,economicandfinancialdataoftheissuer’sregion,whileChinaBond.com.cnprovidesdownloadingofaggregatedatasuchasbondissuance,transactionsettlementandholdermixonthewebsite.Formoredetaileddataandanalysis,oneneedstodownloadsuchproductssuchastheChinaBondDr.Quantfinancialterminal.Dr.QuantprovidesanalyticaltoolssuchasLGBissuance,transactions,outstandings,yieldcurvesandtermstructureineachprovince.ItiscurrentlythemostinformativeLGBanalyticaltoolinChina.TheEMMAplatformintheUnitedStateshasawiderangeofanalyticaltools.Thebondcomparisonfunctionenablescomparisonofbasicbondelements,marketprices,transactiondataandotherinformation.Theissueranalysisfunctionprovidessuchinformationastheissuer’scontactinformation,historicalissuanceandcreditrating.Intermsofexternalextendedtools,investorsareprovidedwithaccesstothird-partyservicesrelatedtothebonds,suchascreditratingsofthebondsassignedbyMoody’s,FitchRatingsandStandard&Poor’s,andthemunicipal-bondmarketyieldcurvesandindicesfromthird-partyproviders.

SeeTable5forthebasicinformationontheLGBdisclosureplatformsofChinaversustheUnitedStates.

SuggestionsonOptimizingLGBInformationDisclosure

Basedontheaboveanalysis,thispaperprovidesthefollowingsuggestionsonoptimizingLGBinformationdisclosure.

i.EnrichingthecontentofLGBinformationdisclosure

Higher-qualityinformationdisclosurewilltranslateintolowerfinancingcostandbetterliquidityofLGBs.InsomepartsofChina,thegranularityofinformationdisclosureshouldbeimproved.ItissuggestedthattheissuerdiscloseadditionalLGBinformationsuchasthepercentageofcompletionoftheproject,useofproceedsandenvironmentalbenefitindicators,soastoreducethefinancingcostthroughhigher-qualitydisclosure.

ii.Unifyingstandardsforinformationdisclosure

IntheactualdisclosureofLGBs,thegranularityofdisclosurevariesacrossregions,andthedisclosurecontentsalsoshowdifferencesbetweenonshoreandoffshorebonds.Therefore,itissuggestedtofurtherimproverelevantlawsandregulations,unifythestandardsforLGBinformationdisclosure,designdisclosuretemplateswithhighergranularityofinformationandimprovetheconsistencyandcomparabilityofdisclosedLGBinformation.

iii.Improvingtheinformationdisclosureplatformfunctions

ThereisstillroomforfurtherimprovementsinthefunctionsofChina’sLGBinformationdisclosureplatforms.Itissuggestedtointroduceadditionalfunctionsofdisclosureplatformsanddisplayauthoritativethird-partyinformationonplatforms,suchasyieldcurvesandpriceindicators,soastofacilitateinvestors’analysisanddecision-making.

Note:

1.“Plan,ReportandOpinion”refertotheImplementationPlanforSpecial-purposeBondProject,theProjectFinancialEvaluationReportandtheProjectLegalOpinion.

References

[1]YaoDongmin,LuoWenqi.ComparativeStudyandOptimalDesignonInformationDisclosureofLocalGovernmentBonds[J].ChinaBond,2023(1):31-38.DOI:10.3969/j.issn.2095-3585.2023.01.008.

[2]ShiXinyi,ChenSuyun.PracticalFoundationandPathforInformationDisclosureofLocalGovernmentBonds[J].CommunicationofFinanceandAccounting,2022(20):14-19.DOI:10.16144/j.cnki.issn1002-8072.2022.20.018.

◇ Authorsfrom:CCDCPost-DoctoralResearchCenter,CCDCShenzhenBranch

◇ Editors:LiaoWenwen,LuNingning